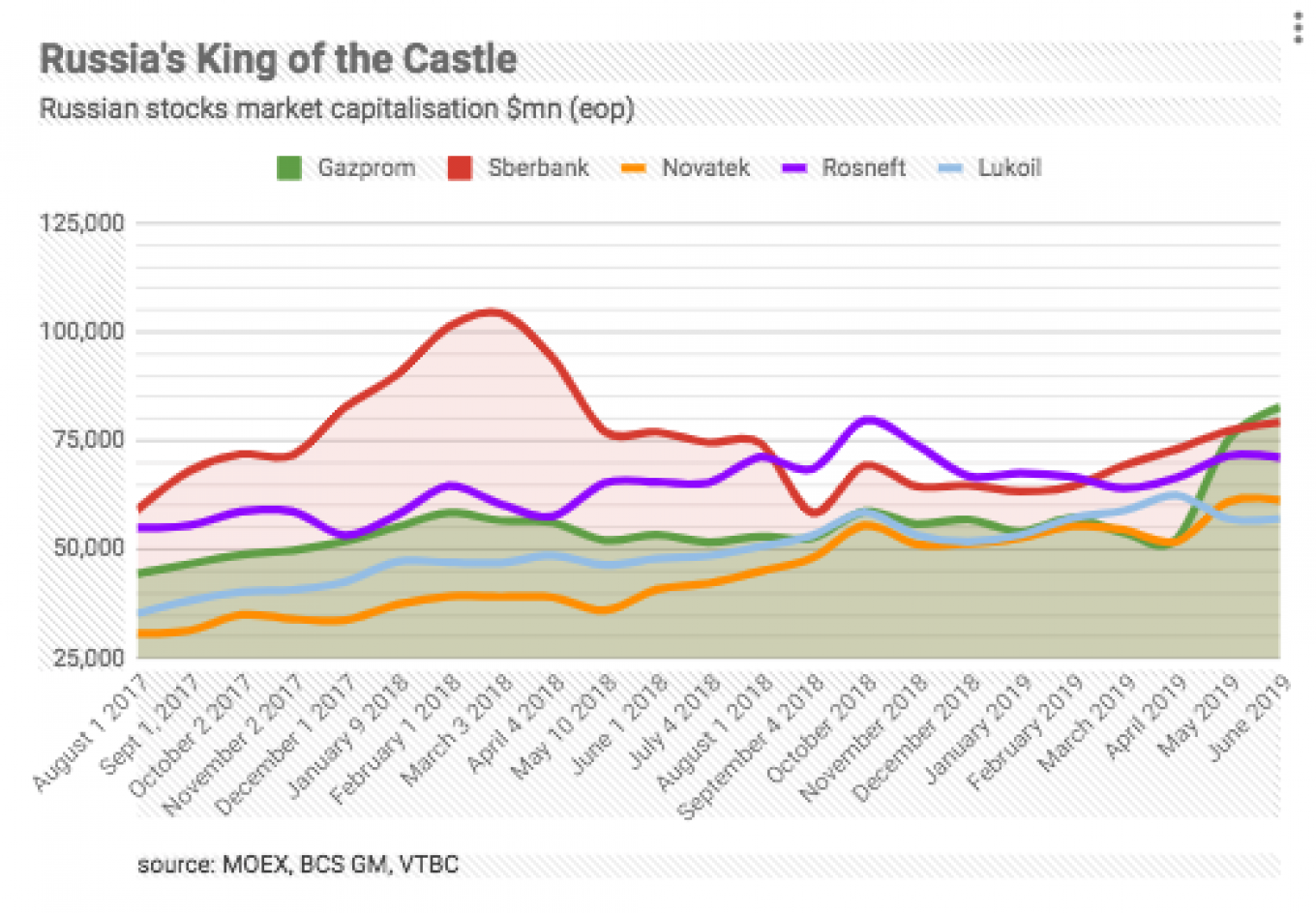

Shares in Russia’s state-owned gas giant Gazprom jumped again, rising by 10 percent in a day to make it Russia’s most valuable company, worth $82 billion, as rumors of the imminent departure of CEO Alexi Miller swirled in Moscow.

Shares in the so-called “state within a state” had already spiked by 30 percent in the last week of May, adding $20 billion to the company’s market capitalisation in a matter of days after the management hiked its dividend twice in a week, effectively doubling the payout to what is now a 27 percent dividend yield.

Shares in Russia’s biggest companies are extremely under-valued because of management’s reluctance to share their profits with shareholders, and their propensity to take spare money and plough it into the ground in the form of never-ending capex programs.

Changes are afoot at the gas behemoth as it has seen several senior managers replaced recently and the government has threatened to take direct control of its massive investment program. Investors have been wondering if the increase in the dividend payout this year is a one-off, but comments from Gazprom since the announcement suggest that something more fundamental is happening.

“The market has reacted positively since the changes in Gazprom’s management and the upward revision to suggested dividends, which, at the time of the announcement, provided for a sizable dividend yield of 10 percent. The company’s commitment (finally) to adopt the new dividend policy by the year-end and its stated intention to move to a 50 percent of international financial reporting standards (IFRS) net income payout in two to three years, have also been welcomed by investors,” Dmitry Loukashov, oil and gas analyst for VTB Capital (VTBC), said in a research note.

“For now, though, we think that the market has started to price in further potential changes in corporate governance, providing “credit” for them to the company in advance,” he added.

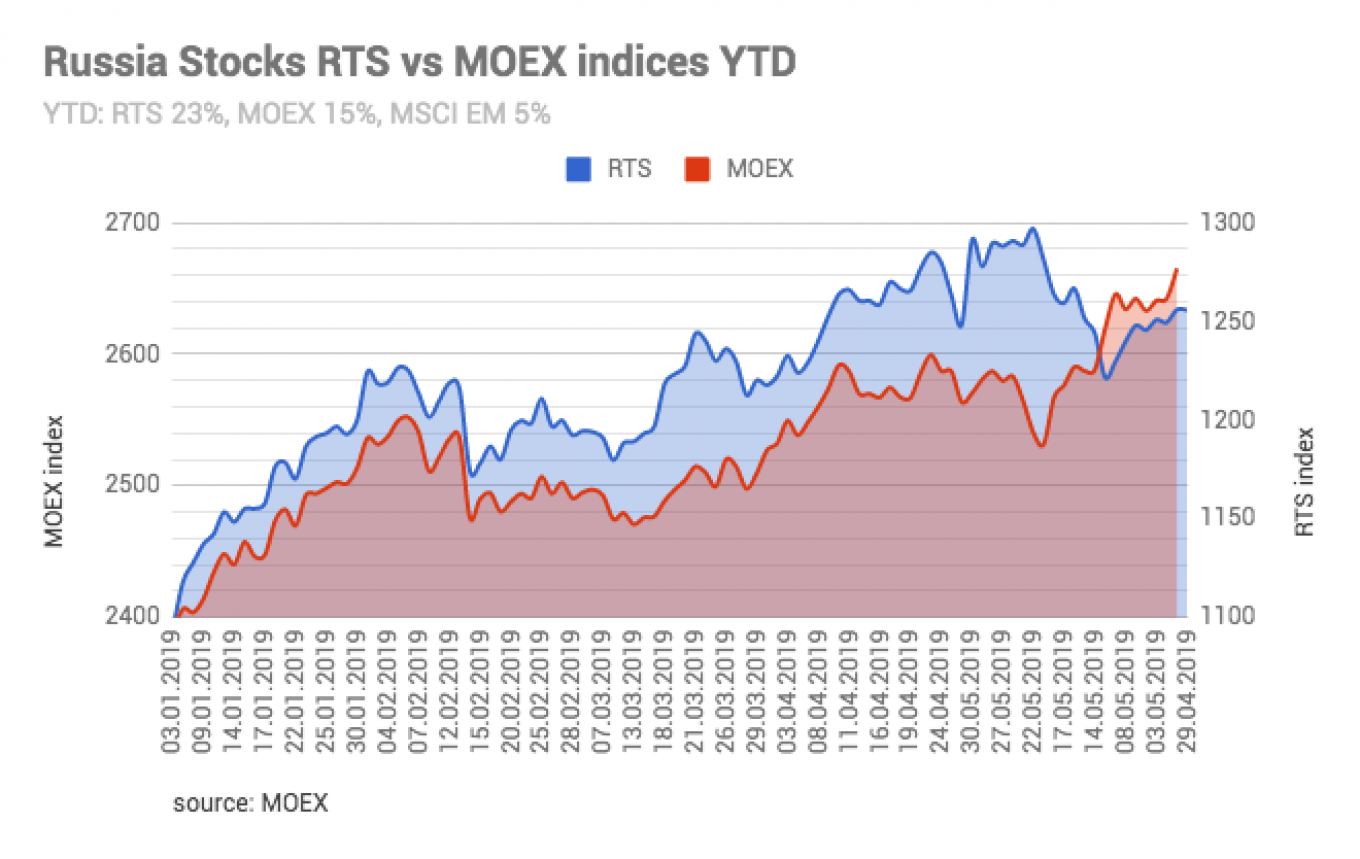

Gazprom shares rose by another 4.14 percent on June 3, driving the market capitalisation of the company to $82 billion (5.38 trillion rubles) and so overtaking the $79.8 billion (5.216 trillion rubles) of Russian state-owned banking giant Sberbank, which had held the title of Russia’s most valuable company for well over a year. Gazprom shares are now up a huge 36 percent from the start of the year, easily outstripping the 23 percent gain the leading RTS index has made in the same period.

As part of the general drive to “transform” Russia’s economy under President Vladimir Putin’s May Decrees and the associated 12 National Projects, the government has also clearly launched a drive to improve the efficiency of its state-owned enterprises (SOEs). Gazprom alone accounts for approximately 10 percent of gross domestic product (GDP), and collectively the SOEs made up the bulk of Russia’s fixed investment in 2018.

Gazprom has been going through a management shake up in recent months as several senior and long-serving officials were replaced in May.

Since the end of February, three deputy chairman of the board have left — Alexander Medvedev (export), Valery Golubev (domestic market) and Andrey Kruglov, (financial unit). In April, Kirill Seleznev, who runs Gazprom Mezhregiongaz’s sales subsidiary, also left the board. He is reportedly one of Miller’s closest allies. Further down the tree, the head of the capital construction department, Sergey Prozorov, and one of the main curators of large-scale purchasing, Mikhail Sirotkin, have also left.

At the same time, Gazprom Vice-Chairman Oleg Aksiutin announced plans to reform the corporate expenditures department, which is responsible for 1 trillion rubles ($15.4 billion) in spending on tenders and procurements. The changes were part of the company’s efforts to avoid losing control over its investments entirely after the government proposed in January to force all of the SOEs to submit investment programs for approval, and effectively take direct control over the capex program.

As part of Aksiutin's drive to improve discipline, a single contractor for Gazprom’s construction program, Gazstroyprom, has already been set up and acquired the main assets of the former largest gas builder Ziyad Manasir. The company is now in talks to buy the construction assets from stoligarchs Arkady Rotenberg and Gennady Timchenko.

VEB (Vnesheconombank) has also reportedly been in talks with Rotenberg and Timchenko to take over their contraction assets as part of the Kremlin’s massive infrastructure spending program under the national projects program. If either of these deals go through it would represent a big change to the way the huge state-backed investments into infrastructure are organised.

Gazprom is Russia’s most unproductive company, according to a study by the World Bank, and was famously used as a piggy bank by its former management under Rem Vyakhirev that stripped billions out of the company for themselves and their cronies in the 1990s. One of Putin’s first big battles after he took over as president in 2000 was to change the management at Gazprom, but now it seems that Miller, who took over, is falling out of favor and the Kremlin is demanding real reforms at the energy giant.

Miller exit

Rumors of Miller’s resignation have been doing the rounds on the market for years, but have become louder since mid-May.

"Speculation on the market that Miller might be on the way out and transferred to run one of the regions has resumed," Citi analysts wrote in a note to clients shortly after the dividends were hiked on May 21, as cited by The Bell.

Investors would be buoyed by Miller’s departure in the hopes that Gazprom’s perennial capex program would finally be curbed, and more cash returned to the government and minority investors in the form of dividends as a result.

Sacking Miller would be a revolutionary move on Putin’s part, almost as significant as his sacking of Vyakhirev, due not only to Gazprom’s economic power, but also the role it plays as a foreign policy tool. Some market participants said the recent spike in the company’s shares was an “insider trading deal” by well-placed government officials hoping to cash in on the further jump in shares that would inevitably follow Miller’s sacking. Government officials buying stocks shortly ahead of major announcements like big rating changes is common in Russia as officials in the know leverage their inside knowledge for profit.

However, rumors aside, the increase in dividends is enough to justify the increase in the share price. Investors have long complained that “investing into Gazprom shares is like buying a bond as the company pays out 8 rubles per share come rain or shine,” Kirill Tachennikov, the oil and gas analyst with BCS Global Markets, told bne IntelliNews in a recent interview.

What investors really want to see is a change in dividend policy that means the company shares more of the billions of dollars a year it makes with investors.

Gazprom reported a 24 percent year-on-year gain in net income under IFRS to $8 billion in the first quarter of 2019, despite revenues and Ebitda declining by 8 percent year-on-year and 13 percent year-on-year, respectively. Its Ebitda beat analysts' forecasts, mostly due to lower gas purchase costs and a sizable $2.8 billion foreign exchange gain, VTB Capital commented on May 31. Gazprom has been selling record amounts of gas to Europe and with three new pipelines about to come onstream — Power of Siberia, Turkish Stream and Nord Stream 2 — its sales will only go up, while its capex should shrink considerably.

In theory that means more cash that can be paid as dividends to shareholders. The management promised as much during a conference call last week after the release of results. The company said it is now working on a new dividend policy that it expects to finalize and submit to the board of directors for approval by the end of this year. Moreover, it promised that the payout ratio of 50 percent is "likely to be the ceiling in the new dividend policy," as cited on May 31 by Sberbank CIB, but also said the new 16.6 ruble per share was now a floor for future dividend payments.

This article first appeared in bne IntelliNews.

A Message from The Moscow Times:

Dear readers,

We are facing unprecedented challenges. Russia's Prosecutor General's Office has designated The Moscow Times as an "undesirable" organization, criminalizing our work and putting our staff at risk of prosecution. This follows our earlier unjust labeling as a "foreign agent."

These actions are direct attempts to silence independent journalism in Russia. The authorities claim our work "discredits the decisions of the Russian leadership." We see things differently: we strive to provide accurate, unbiased reporting on Russia.

We, the journalists of The Moscow Times, refuse to be silenced. But to continue our work, we need your help.

Your support, no matter how small, makes a world of difference. If you can, please support us monthly starting from just $2. It's quick to set up, and every contribution makes a significant impact.

By supporting The Moscow Times, you're defending open, independent journalism in the face of repression. Thank you for standing with us.

Remind me later.