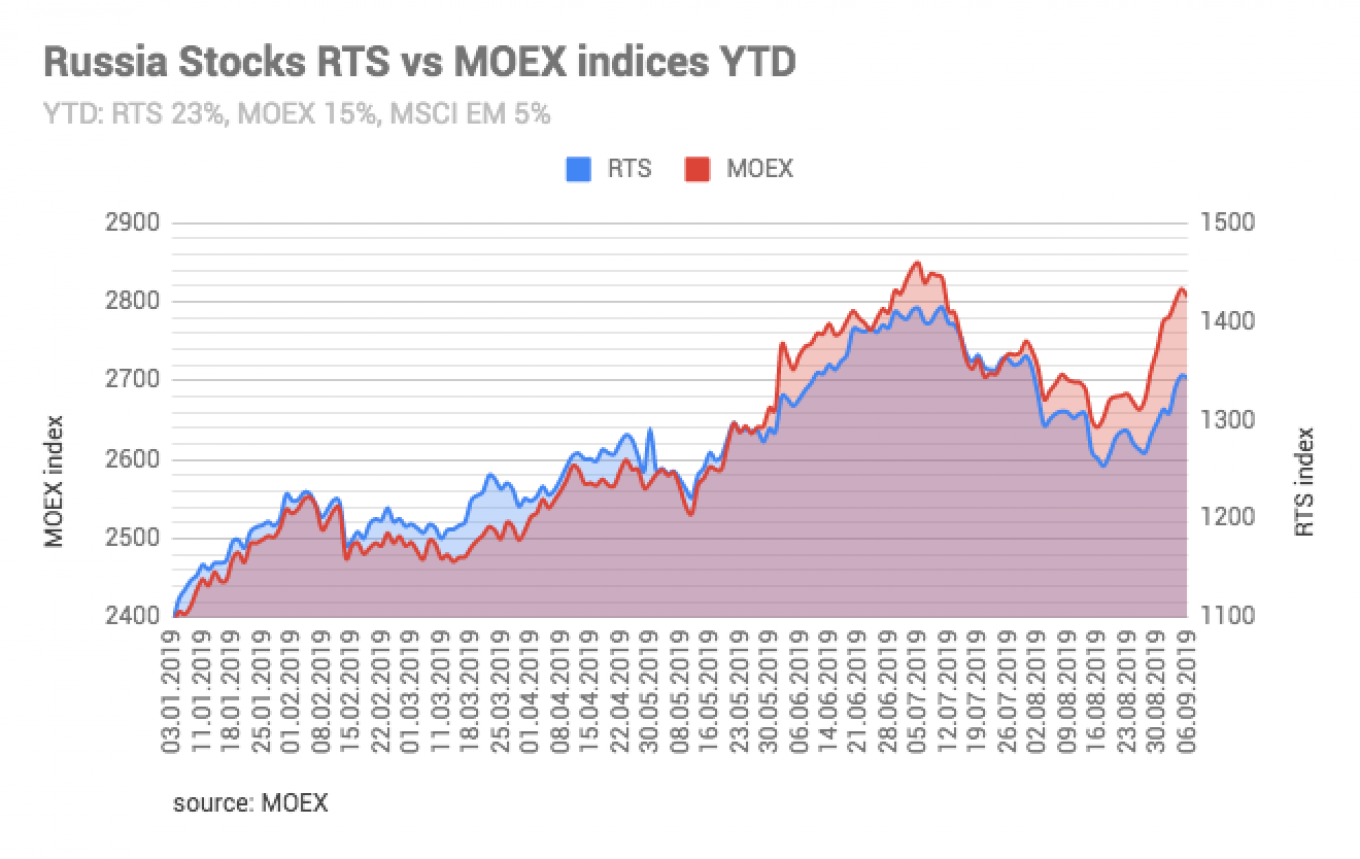

Russia’s stock market rallied in the second quarter of this year, up some 30% since January, and broke through the 1,400 level briefly in June for the first time since the annexation of Crimea in 2014. Stocks have rallied strongly this year but the outlook for the rest of the year is hazy and investors are only looking at a few names rather than the market as a whole.

The outlook for Russian stocks should be good. Both the banking sector and the corporate sector are making the best profits seen since the onset of sanctions as the economy is clearly recovering, at least as far as listed companies are concerned, even if the macroeconomic growth remains subdued.

“Russian stocks are among the best performers year-to-date across emerging markets. The MSCI Russia has gained +30% year-to-date, holding its position as one of the leaders in the EM space. The RTS index tested the 1,400 level in June, returning to the area near our base case full-year 2019 target of 1,250 in August. We keep that target unchanged, since the biggest drivers of Russia’s outperformance, corporate governance improvements and sanctions sentiment dissipation, lack further triggers,” VTB Capital (VTBC) said in a note.

This year is turning out to be “a game of two halves” for the financial markets, according to VTBC. “The first half of the year featured a decent equity market performance, bolstered by expectations of an early resolution to trade disputes and above-trend growth. The sell-off in the second half of the year was triggered by the Fed’s unclear approach to looser policy and the increased trade tensions that are raising global recession risks,” VTBC said in a note on the equity market outlook.

At home the Russian economy is looking stronger as companies get back on their feet and demand recovers, albeit largely driven by consumer credit rather than rising incomes. But the deteriorating external environment is weighing on sentiment and makes this year’s outcome unpredictable.

The main issue that investors are grappling with is the escalating showdown between Washington and Beijing, which has superseded the Russia-U.S. face-off as the main geopolitical confrontation. Indeed, since the release of the Mueller report earlier this year that concluded there was “no collusion” between the Kremlin and the White House, the wind has gone out of the Russia-hysteria’s sails and Beijing has come to replace Moscow as the focus of the xenophobic “enemy at the gate” rhetoric that has become a feature of U.S. domestic politics.

And the tensions are rising. U.S. President Donald Trump’s trade war with China has escalated into a “currency war” after the Chinese devalued the yuan in August, only to face $400 billion worth of new trade duties in retaliation. Central banks around the globe, having embarked upon easing cycles, now find themselves with far less ammunition to fight currency fluctuations than during the 2007-08 financial crisis. Indeed, as most countries are still running near-zero interest rate policies and everyone — with the very noticeable exception of Russia — has debt to GDP ratios of around 100%, if there is another global financial crisis none of the major global economies has much left in reserve, in terms of capacity for emergency rate cuts or borrowing, to fight against a deep recession.

The irony of the sanctions policy against Russia is that it has left it the best prepared to deal with any turmoil, should there be a debt-led global crisis. And with bond yields turning negative around the world, a debt-led crisis is now a distinct possibility.

In the meantime, portfolio investors are focused on the more immediate ebb and flow of sanctions rhetoric. The second-quarter rally was driven by the ebb of sanctions talk, whereas the profit-taking in July and August was a result of a return to tougher sanctions talk. The eventual release of the second round of sanctions related to the poisoning of ex-spy Sergei Skripal ended up being symbolic — placing a few restrictions on U.S. investors buying Russian sovereign primary issues, but not banning them from either owning this debt nor buying it on the secondary market — and equities rallied in relief.

But underpinning the geopolitical machinations is the continued progress amongst Russia’s leading corporates, who have been forced by the quiet crisis of the last few years to turn inwards, cut their capex and improve efficiency and profitability, and the general trend in improving corporate governance amongst most of the leading blue chips. The fact that the average Russian dividend yield is twice as large as the benchmark MSCI emerging market average, oscillating between 7-7.5% versus the 3.3% MSCI average, also adds to the appeal of Russian stocks.

Given the uncertainties, VTBC is keeping its end of year target for the RTS at 1,250, which is actually less than the 1,340 it was trading at as of Sept. 5. These prices massively undervalue Russian stocks compared to their emerging market peers, making Russian equities some of the cheapest in the world. The MSCI Russia 12-month forward price-to-earnings ratio (p/e) ratio (a standard measure of the attractiveness of a stock) continued to oscillate below 6.0x, but fell to 5.7x in August. The p/e ratios of other emerging markets are typically in the mid- to high teens.

Bottom up things look better

Not only has the equity market been a story of two halves this year it is also a story of two views: the aggregate market picture is moribund, however, looking at the market bottom up from the point of view of stocks that are likely to outperform, the picture is very different.

The consolidation that has gone on in various sectors and their reaction to the ongoing recovery means individual names have seen their share prices soar.

While the VTBC outlook of 1,250 for the RTS suggests a small retreat this year, the outlook for the best stocks has a 17% upside for the rest of the year.

The idiosyncratic nature of these gains is highlighted by the fact that 53% of these gains are concentrated in the outperformance expected from a single stock – Sberbank, currently Russia’s “tourist stock,” the first name that anyone with an interest in Russian equity always buys. Analysts calculated that the upside to Sberbank’s stock current price is a whopping 64%.

If you add the other top names of Gazprom and Lukoil to this calculation, accounting for another 35% and 21% in VTBC's “bottom up” portfolio of top picks, then the bulk of the exposure to Russia’s equity is concentrated in three names. Gazprom’s stock has already gained 74% year-to-date, following a spike in its share price after the management unexpectedly doubled its dividend payout in May. Surgutneftegaz’s share price also jumped 20% in a day in the first week of September after the management hinted it would move some of its famous $50 billion cash pile into a fund and could actively invest it. (Currently no one is sure where this money actually is. Some speculate it is on deposit with the state-owned banks. Moving it into a fund might give investors into Surgut’s shares access to profits this fund may earn.)

Global problems growing

The mismatch between the outlook for the overall index and the outlook for the individual stories is reflected in the darkening outlook for the global economy in the next year. The chance of a global recession is rising quickly, according to analysts, as a series of pressures have come together to push down growth and confidence.

PMI contracting

Currently, 17 out of 30 countries in the global PMI manufacturing index are in contraction territory. The global index is at its lowest level since October 2012. In the U.S., the PMI manufacturing index slipped into contraction for the first time since 2009. The eurozone PMI manufacturing index has been in contraction territory since February, with Germany flirting with recession. Asian PMIs are also negative. The Chinese PMI data remains indecisive in spite of significant credit expansion over the past year or so, accompanied by a targeted fiscal expansion. The deterioration in global trade flows continues to accelerate, with global exports falling for a twelfth consecutive month as of August. The recent Chinese currency devaluation adds to global economic uncertainty and turns a “trade war” into a “currency war.” The consequences for the global economic outlook are clearly negative.

‘Japanification’ of inflation

Persistent inflation is starting to convince central banks around the world that this is not a short-term phenomenon and the global economy is facing the risk of the ‘Japanification’ of inflation, similar to the long-term low growth and low inflation that besieged the Japanese economy after its crash at the start of the 90s. Indeed, some countries – most noticeably the US Federal Reserve bank – have reserves tightening policies and are now easing again as growth slows.

“Now, central banks find themselves in an unusual situation a decade after the financial crisis of 2007-08. The Fed has less interest rate ammunition while the European Central Bank and Bank of Japan have completely failed to ‘normalize’ interest rate policy. Moreover, there is only so much that monetary policy can do amid unprecedented trade wars,” VTBC said in a note. As the interest rate cut ammo has nearly all been used up the next round of aid will probably come in the form of fiscal stimulation and both the US and German are already talking about plans.

Trade wars

Trump's bull in the china shop approach to trade relations is causing significant damage to global trade and growth and is unlikely to be wound down anytime soon, which is also hurting global growth. More locally Brexit is having a similar effect in Europe with all the major economies, and especially those in Central Europe, in the firing line. The restrictions on Russia thanks to the sanctions regime are also constraining its growth and have cut at least 2 percentage points off its growth as the Ministry of Finance and Central Bank of Russia have adopted a war mentality to ensure the safety of the economy from more economic assaults rather than encouraging growth.

This article first appeared in bne IntelliNews.

A Message from The Moscow Times:

Dear readers,

We are facing unprecedented challenges. Russia's Prosecutor General's Office has designated The Moscow Times as an "undesirable" organization, criminalizing our work and putting our staff at risk of prosecution. This follows our earlier unjust labeling as a "foreign agent."

These actions are direct attempts to silence independent journalism in Russia. The authorities claim our work "discredits the decisions of the Russian leadership." We see things differently: we strive to provide accurate, unbiased reporting on Russia.

We, the journalists of The Moscow Times, refuse to be silenced. But to continue our work, we need your help.

Your support, no matter how small, makes a world of difference. If you can, please support us monthly starting from just $2. It's quick to set up, and every contribution makes a significant impact.

By supporting The Moscow Times, you're defending open, independent journalism in the face of repression. Thank you for standing with us.

Remind me later.