The Russian ruble rose to a two-week high on Tuesday after the government and the Central Bank put pressure on large state-owned exporters to sell dollars to stop further steep losses for the local currency.

In mid-December, the ruble plunged to its lowest level since the financial crisis of 1998 on the back of lower oil prices and Western sanctions, which make it almost impossible for Russian firms to borrow from the West.

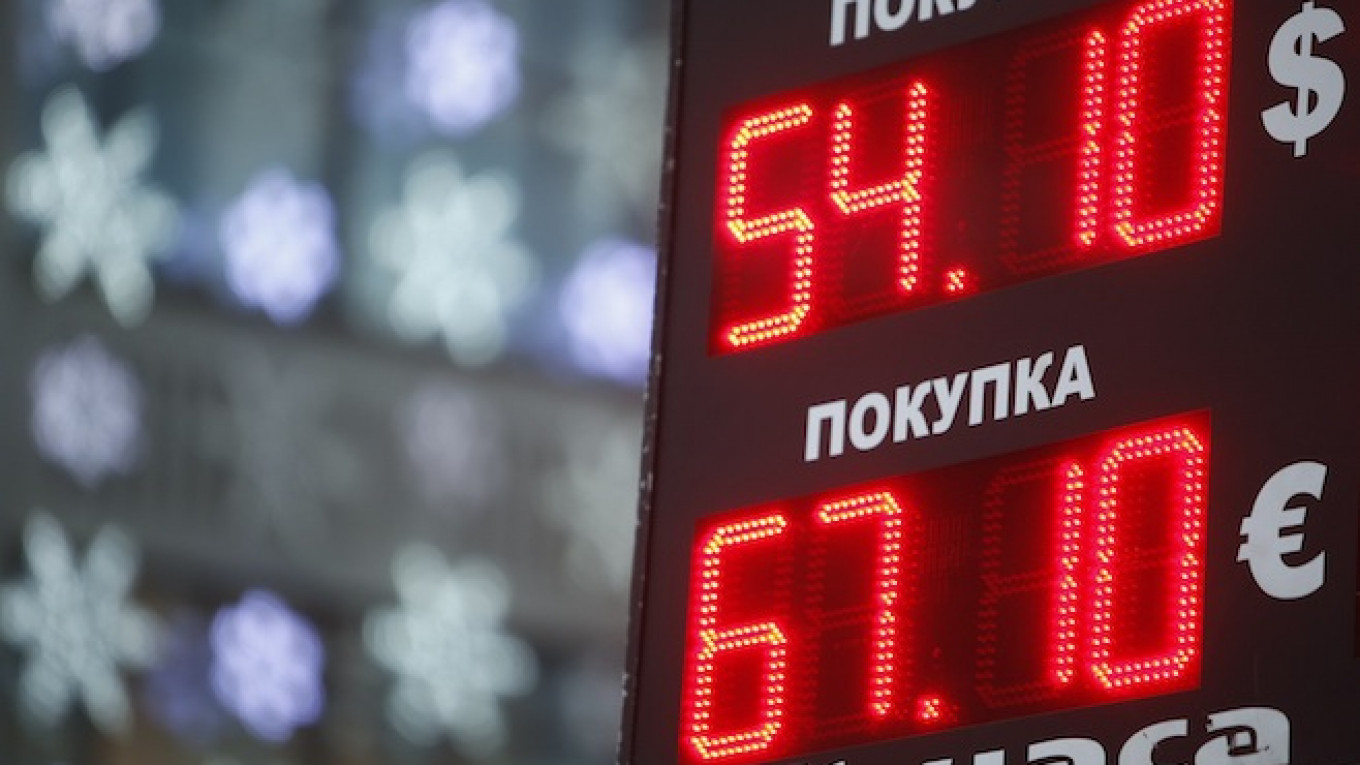

The ruble fell to as low as 80 per dollar this month, from the average of 30-35 seen in the first half of the year, but has recovered since to trade as high as 53 to the dollar on Tuesday.

Kommersant newspaper said, citing unnamed sources, that Russian Prime Minister Dmitry Medvedev had signed an order obliging the country's largest state exporters to sell part of their foreign currency revenues.

The paper said that in the next two months, companies may provide the market with about $1 billion per day in total dollar sales.

The Central Bank said in a statement it was conducting consultations with large exporters with the aim of stabilizing the currency market.

President Vladimir Putin has repeatedly promised not to reintroduce capital controls but the new measures are likely to be seen as a softer version of restrictions on capital flows.

The exporters also have to pay tax bills at the end of the month that require them to convert foreign earnings into rubles. The peak of their tax payment is expected on Dec. 25.

Shortly after the market opening, the ruble hit 52.88 against the dollar — its strongest level since Dec. 8.

By 11:22 a.m. in Moscow, it was up 1 percent at 55 to the dollar.

A Message from The Moscow Times:

Dear readers,

We are facing unprecedented challenges. Russia's Prosecutor General's Office has designated The Moscow Times as an "undesirable" organization, criminalizing our work and putting our staff at risk of prosecution. This follows our earlier unjust labeling as a "foreign agent."

These actions are direct attempts to silence independent journalism in Russia. The authorities claim our work "discredits the decisions of the Russian leadership." We see things differently: we strive to provide accurate, unbiased reporting on Russia.

We, the journalists of The Moscow Times, refuse to be silenced. But to continue our work, we need your help.

Your support, no matter how small, makes a world of difference. If you can, please support us monthly starting from just $2. It's quick to set up, and every contribution makes a significant impact.

By supporting The Moscow Times, you're defending open, independent journalism in the face of repression. Thank you for standing with us.

Remind me later.