The consumer debt profiles of Russia and Ukraine are very different.

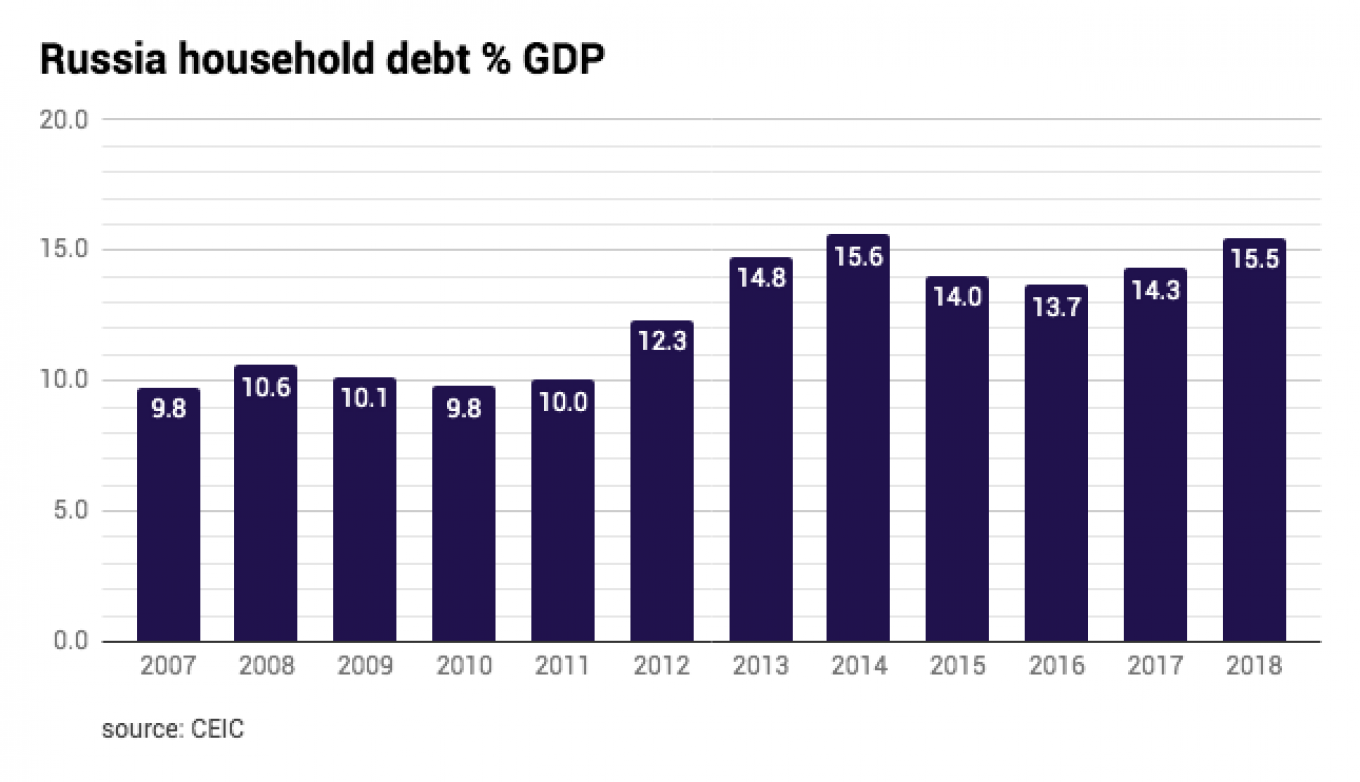

Russia’s household debt had risen to 15.5% of GDP as of the end of 2018 and is just shy of its all time high of 15.6% set in 2014.

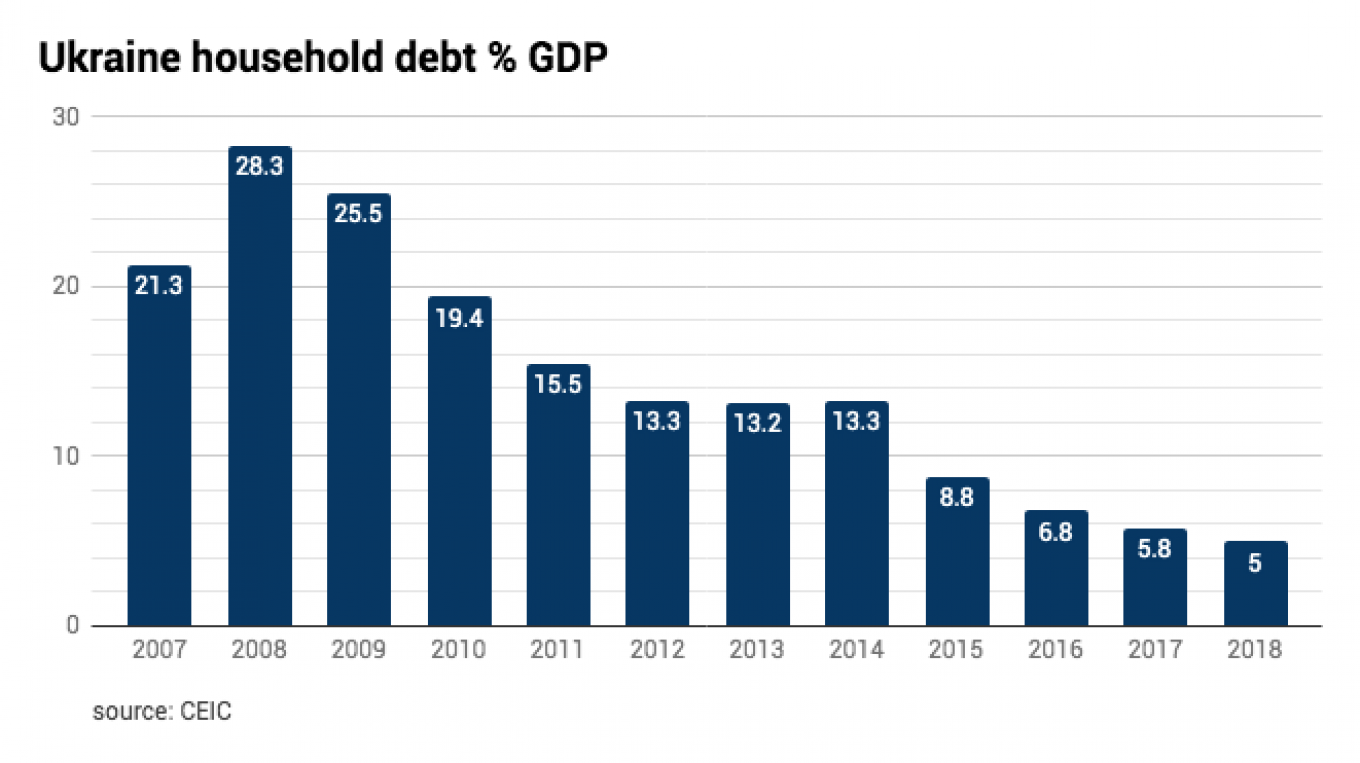

Ukraine’s household debt has been falling steadily from its all time high of 28.3% set in 2008 and is now around 5%, according to official figures, setting the economy up for a consumer credit driven retail boom in the future.

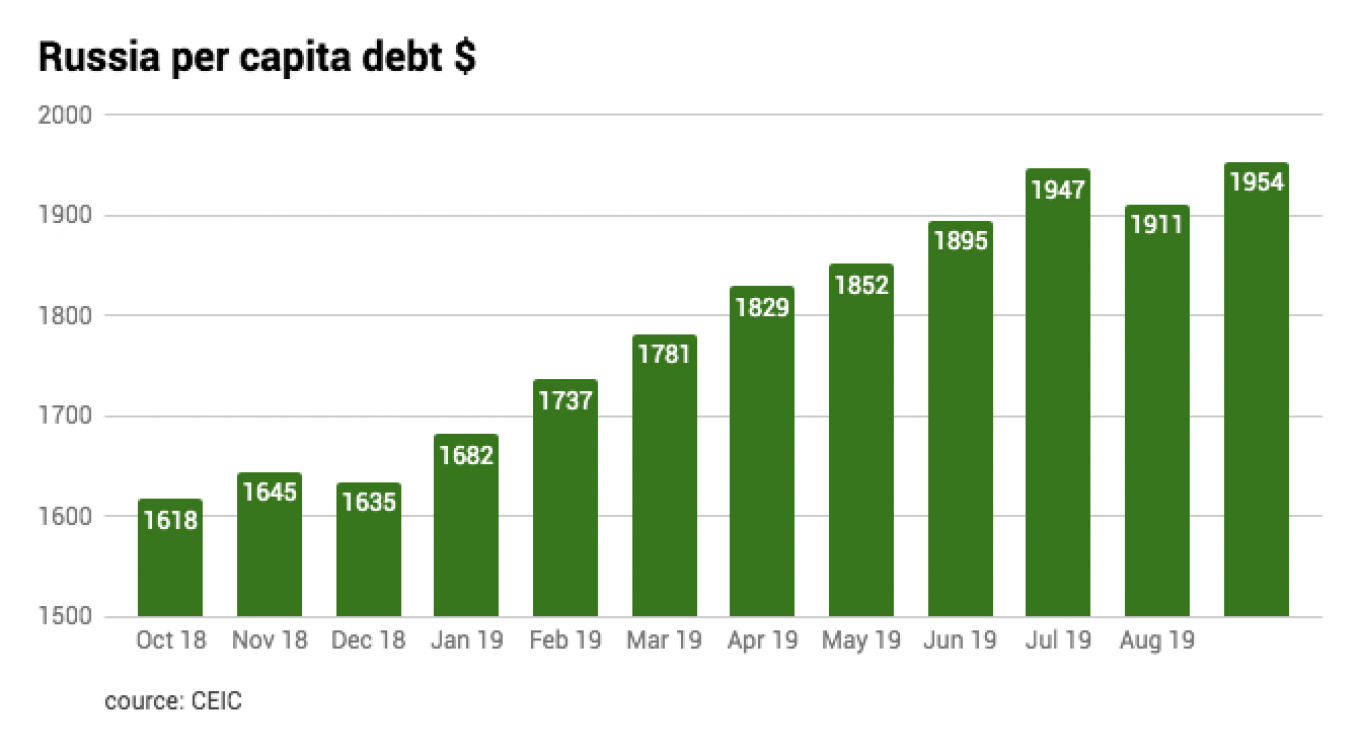

There is a big difference too in the dollar values of the debt. Russia’s per capita household debt has increased by $336 in the last year to $1,954 per capita as of September this year, which is slightly more than the equivalent of two months’ salary.

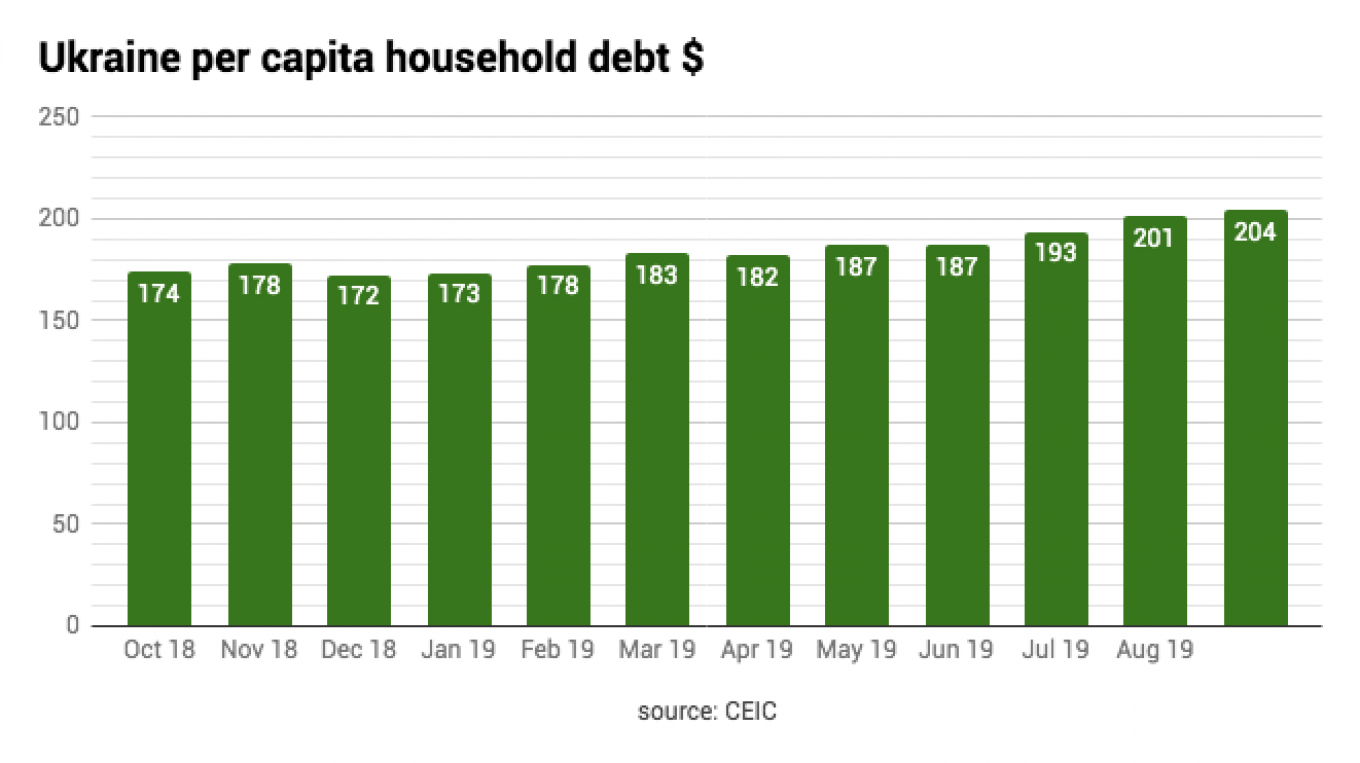

Conversely, Ukraine’s per capita household debt has also crept up in the last year, but only by a modest $30 to $204 per capita, which is slightly more than half a month’s salary.

In both countries these debts are still small enough that if a debtor gets into trouble and loses their job it is possible to pay the debts off by calling on friends and family. However, in Russia’s case, the burden of debt is starting to reach a point where covering it is becoming more and more difficult.

A debate has been raging in Russia over the dangers of the rising consumer indebtedness. Consumer borrowing has been rising by 25% per year, but more recently as Russia’s central bank starts to tighten the prudential rules surrounding retail loans the rate of growth has fallen, dropping to 21% as of the third quarter.

However, double-digit loan expansion compares to growth of nominal incomes of 6.8% and of real income growth of 3.3% in September, meaning the debt pressure on consumers is slowly increasing.

Russia has almost used up its immediate capacity to fuel economic growth via retail loans and consumption. Economists say that in the last two quarters most of the growth has been driven by consumption, and that was largely paid for by credit as the propensity to save has also fallen. Russians, it seems, have got fed up with being poor and have started to borrow more to fund their previous standards of living.

The tightening screws on borrowing and real incomes in Russia have been on the decline for six years now and are weighing on retail turnover which slowed to 0.7% growth in September, down from 0.8% a month earlier.

In Ukraine, the very low levels of household debt mean the economy has significant capacity to enjoy a consumer credit-led retail boom similar to that which Russia enjoyed for most of the noughties that fuelled economic growth of 6-7% per year.

While Ukraine’s banks have not yet turned to retail as a main source of business, with real wages growing by 9.8% in September and retail turnover growth of 8.6% in the same month, clearly the conditions for a sustained boom are in place.

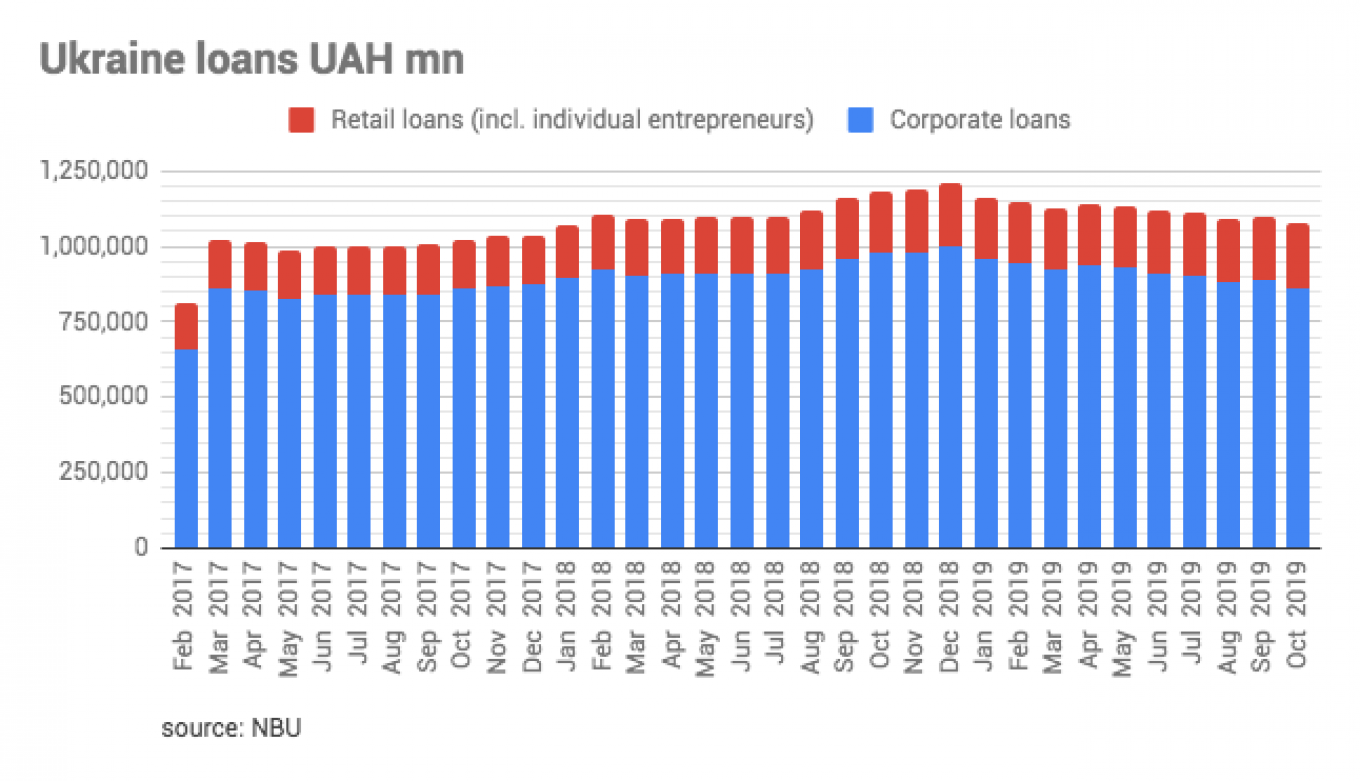

The banking sectors of both countries are in good shape as central banks in both countries have carried out very successful clean-up operations. However, with a significant non-performing loan (NPL) overhang in Ukraine — just under half of the aggregate loans on banks’ books are non-performing — Ukraine’s banks are being very cautious and focusing mostly on corporate loans

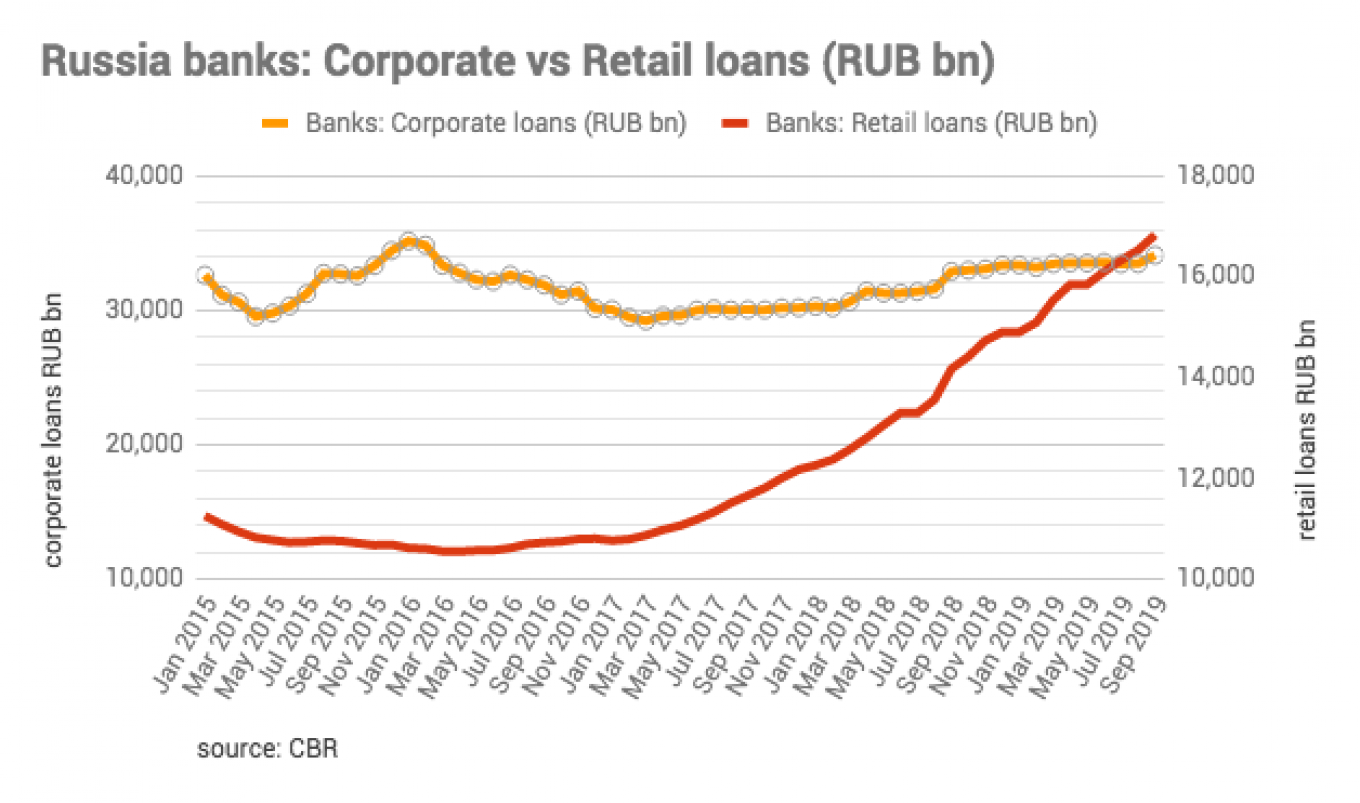

In Russia, while retail loans remain at half the volume of corporate loans, the high profitability of this business and the significant investments all banks have already long since made in building up a retail franchise means the volume of retail lending continues to rise quickly — especially in light of the fact that the corporate lending business has been largely stagnant for about four years.

Following the collapse of oil prices in 2014, and the deep devaluation that followed, Russia’s companies have mainly been focused on deleveraging, not taking out new debt.

Corporate lending is not booming in Ukraine either, but there the problem is bankers complain there are so few high quality clients to lend to that also want to borrow.

The fact that Ukraine’s monetary policy rate is a very high 15.5%, even after a full percentage point cut this month, also makes commercial debt unattractive.

On this score, Russia is in a better place as the Bank of Russia also dramatically cut rates by 50 basis points this month to 6.5%, and more cuts are expected, making commercial borrowing a lot more attractive, but owners are suffering from a crisis of confidence which has kept borrowing low and dividend payouts high.

This article first appeared in bne IntelliNews.

A Message from The Moscow Times:

Dear readers,

We are facing unprecedented challenges. Russia's Prosecutor General's Office has designated The Moscow Times as an "undesirable" organization, criminalizing our work and putting our staff at risk of prosecution. This follows our earlier unjust labeling as a "foreign agent."

These actions are direct attempts to silence independent journalism in Russia. The authorities claim our work "discredits the decisions of the Russian leadership." We see things differently: we strive to provide accurate, unbiased reporting on Russia.

We, the journalists of The Moscow Times, refuse to be silenced. But to continue our work, we need your help.

Your support, no matter how small, makes a world of difference. If you can, please support us monthly starting from just $2. It's quick to set up, and every contribution makes a significant impact.

By supporting The Moscow Times, you're defending open, independent journalism in the face of repression. Thank you for standing with us.

Remind me later.