Last week President Vladimir Putin celebrated 20 years in power. We take a look at how the country has been transformed under his leadership by going through the numbers.

On Aug. 9, 1999, Putin was plucked from obscurity and made prime minister. A short six months later Boris Yeltsin stepped down as president and Putin moved smoothly into his place.

That had always been the plan. Russia was still reeling from the aftershocks of the collapse of the Soviet Union and the 1998 financial crisis that saw Russia default on some $40 billion worth of GKOs, or federal treasury bonds, that had been snapped up by foreign investors, and the collapse of most of the major banks.

Russia was beleaguered by what academics Barry Ickes and Clifford Gaddy had dubbed “the virtual economy.” The payment system had collapsed as a result of hyperinflation that wracked the country after prices were liberalized by Russia’s first post-Soviet prime minister Yevgeny Gaidar and business was done on barter.

GDP growth had been negative for a decade, bar a few months in 1998. The government was in a permanent budget crisis. Poverty had soared as life expectancy and incomes plummeted. Our “despair index” (the sum of the inflation and unemployment rates added to the share of people living in poverty) had hit the astronomical value of 1440 — ten times worse than any other country in the former socialist bloc.

However, Putin was incredibly lucky. The 1998 crisis was caused by the collapse of oil prices on the back of an Asian crisis a year earlier. But by 2000 oil prices began to recover from their low of $10 per barrel and over the next decade climbed inexorably to a peak of about $150. The flood of petrodollars made rebuilding Russia much easier, but to his credit Putin didn't squander the money but used it to build a new country.

Putin was responsible for the first systematic attempt to reform Russia’s economy. In 2000 he launched the so-called Gref plan (“Programme for the Socio-Economic Development of the Russian Federation for the Period 2000-2010”), named after the then economics minister and now Sberbank CEO German Gref. But the plan was abandoned when the 2008 crisis struck when it was only 30% complete. There was a lot of stealing during Putin's first term in office, but real progress was made, leaving Russia’s economy far ahead of the rest of the Commonwealth of Independent States (CIS).

The numbers paint a clearer picture of the mixed results as the job of turning Russia into a modern and efficient market economy is far from over. Below we pick out the main indicators and divide them into three main categories: macroeconomic, social and quality of life.

'Macroeconomic'

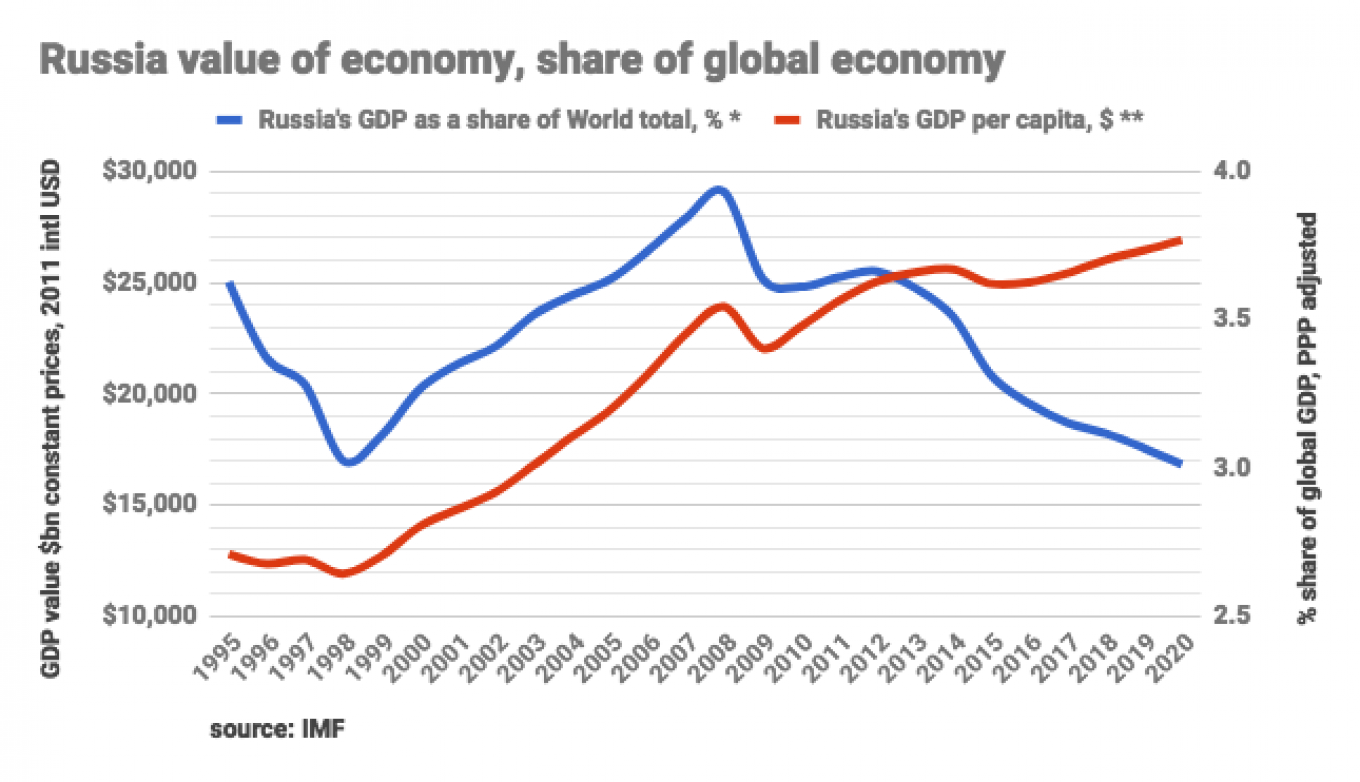

Size and share of Russia’s GDP

The Russian economy is big, but the collapse of the Soviet Union saw its value and share of the global economy collapse. Most of that collapse happened on Yeltsin’s watch, but as the chart shows, Russia’s share of the world’s economy rapidly recovered after Putin took over, rising from about 2% to about 4%. The global financial crisis of 2008 brought that process to an end and Russia’s economy clearly began to stagnate after 2013, a slowdown made worse by the collapse of oil prices in 2014.

In the 10 years from 1999 to 2008, Russian GDP grew by 94% and per capita GDP doubled. The value of the economy rose from $210 billion in 1999 to a peak of $1.8 trillion in 2008. The crisis knocked the value back to $1.2 trillion and with the stagnation now the economy is not expected to get back to $1.8 trillion until 2023.

Looking at Russia's share in global GDP, Russia has returned to where Putin started in the late 1990s. Russia's role in the global economy was at its peak in 2008, but Russia is now in danger of getting left behind as the rest of the world grows faster than Russia does.

GDP growth

There was no growth under Yeltsin. The economy contracted for a decade. But that changed suddenly and dramatically after Putin took over. One of the benefits of the 1998 crash and devaluation was it re-monetized the economy and killed off the “virtual economy.” As people went back to using cash and the petrodollars started to flood in the economy boomed. GDP growth in 2000 was 10% as the economy bounced back from the crash — a record yet to be beaten. The two crises in 2008 and 2014 were major shocks to the economy.

Booming growth before 2008 mainly reflected rising standards of living and consumption on the back of high oil prices. After 2014 consumer demand was stagnant and fixed investments were negative too as Russia’s economy moved into a post-oil boom phase where it ran up against deep structural problems.

Russia is now in its fourth phase of post-Soviet transformation (first: Yeltsin’s 1990s collapse; second: oil-driven noughties boom; third: economic stagnations from 2013 after the oil-model was exhausted) where Putin’s May Decrees and the 12 national projects are attempting to create a new economic model driven by supply-side investment, not demand-side consumption that drove the growth in the noughties.

Economic Reform Plans

Under Putin there have been several attempts at reform, most of which have failed.

The first was the Gref plan launched shortly after he took office that was ended by the 2008 crisis.

The next was the Concept for the Long-Term Socio-Economic Development of the Russian Federation until 2020, but thanks to the global crisis it was never implemented.

In January 2011, Putin instructed the Higher School of Economics and the Presidential Academy of National Economy and Public Administration to create a new Strategy 2020, which resulted in the so-called first round of the May Decrees in 2012, signed on May 7 that year.

The result of the first round of May Decrees did little to reverse the slide into stagnation, so they were replaced with a new round of May Decrees in 2018 that have been augmented with the 12 national projects that are the latest version of the plan to transform Russia’s economy.

Natural resource rents

Russia is blessed with almost every known mineral and natural resource known to man. Oil and gas exports are the most important of those and the government has been able to earn rents from this business that paid for much of the transformation.

Putin's rise to power coincided with resource rents skyrocketing in the early 2000s. But resource rent has been declining in the past years after peaking in 2006-2008. It means that the pie is shrinking and internal conflicts between different factions are rising.

Size and share of grey economy

The size of Russia’s grey economy today is estimated to be 34% by the IMF and hasn't really changed much over the last 20 years. However, under Yeltsin the idea of a grey economy was fairly meaningless as most of the economic activity was done on barter so tax payments were an irrelevance, which fueled the ongoing crisis. Since Putin took over the tax authorities have been rationalized and in the last two years Russia has seen a tax revolution with massively improved efficiency.

Russia still has a high share of informal economy. The state has been trying to put an end to the practice of wages in envelopes and to make informal sector workers pay taxes and social contributions, without a lot of success.

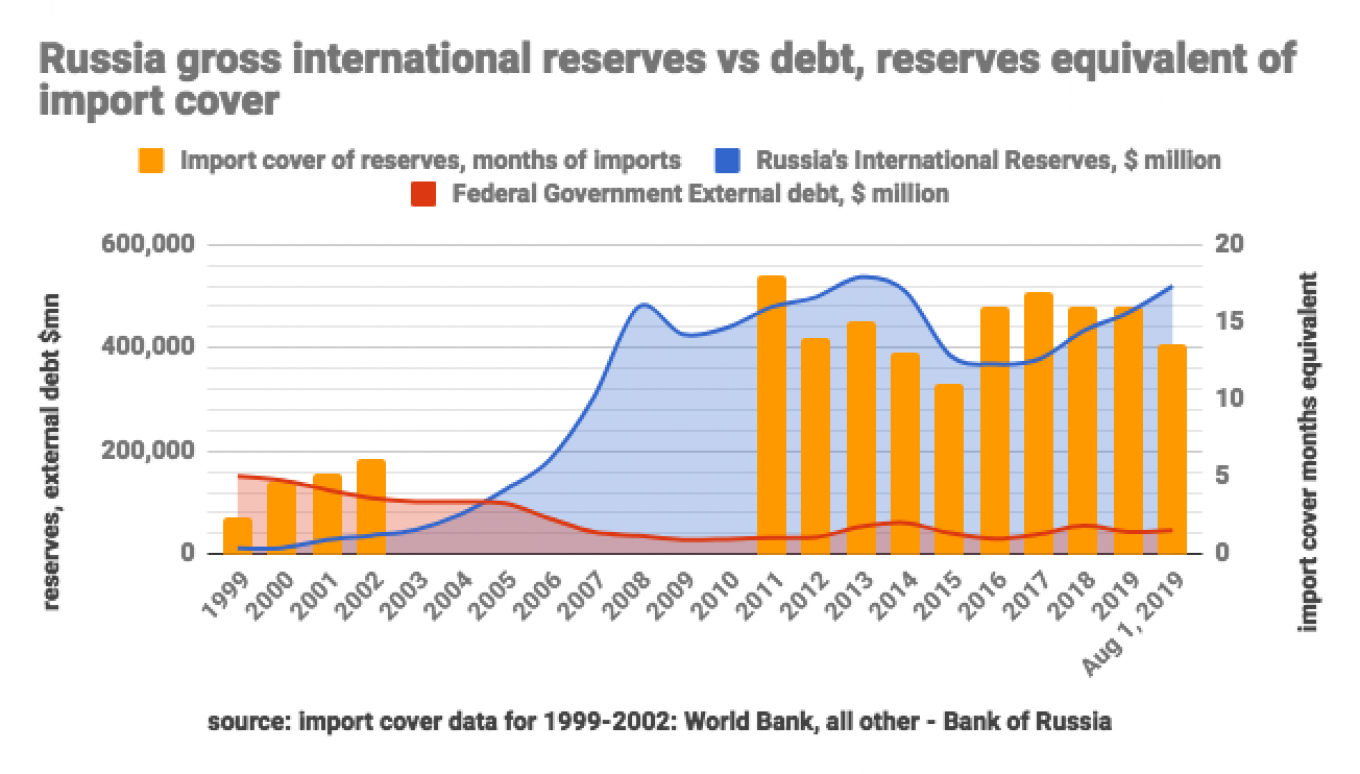

Reserves, external debt and import cover

The flood of petrodollars that arrived in the noughties have transformed Russia’s finances. When the 1998 crisis happened Russia had a mere $10 billion of international reserves, which was enough to pay for two and half months of imports — less than what economists believe is needed to ensure the stability of the national currency.

But as the noughties wore on the government prudently squirreled away the excesses into various rainy-day funds. Even after the stagnation set in from 2013 the state has prudently maintained these very high levels of reserves in anticipation of more shocks, and more recently in anticipation of more sanctions.

Reserves peaked in 2013, about a year before the Crimea's annexation and the onset of the conflict over Ukraine. In the following years they declined because of the Central Bank of Russia's (CBR's) interventions to support the ruble, a policy it abandoned in late 2014, and the Finance Ministry's Reserve Fund spending to cover fiscal deficits.

The fall of Russia’s federal external debt as a share of its reserves is so extreme that you have to use a logarithmic scale to capture the change: external debt fell from 1,243% of reserves in 2000 to 8.9% today.

Russia's international reserves have exceed the federal and central government foreign debt since 2005 and this year reserves cover Russia’s entire external debt dollar for dollar in cash. Reducing debt has been a core part of Putin’s financial policy. Among the first things he did as president was repay the IMF's '90s loans early in 2005.

Federal budget oil and gas revenues

In the 90s the government lived off the revenues it earned from gas exports. Gazprom was regularly hit with “special” tax payments to stave of budgetary crises. However, the deep devaluation of the ruble in 1998 transformed the oil business overnight, making it widely profitable. The leading oil companies invested more in 1999 than they had invested in the previous decade. As oil prices soared, oil revenues became progressively more important to the budget.

Oil and gas revenues of the federal budget rose spectacularly since early 2000s and peaked at over 50% in 2012-2014. Their share is still high (and would be even higher if we calculate general taxes in the oil and gas industry and some other non-tax proceeds)

Federal budget VAT revenues

As Russia’s economy began to function normally the other major source of revenue has become VAT, which now accounts for a third of the government’s income — on a par with, and some times more than, oil and gas revenues. That’s why the decision to hike VAT by 2 percentage points at the start of this year was a big deal; although highly unpopular, it shores up the government’s finances and reduces its dependence on oil and gas prices.

Federal budget deficit

Again the division between the boom years, when the Russian budget ran a healthy surplus, and the stagnation years where the budget has been in deficit, is very clear. However, following deep reforms to the tax service and a huge improvement in tax collection, coupled with a modest rise in oil prices, the federal budget is back in surplus. In the boom years oil prices had to be $115 for the budget to break even; now they need to be $43. The make-up of the budget has been transformed.

Federal budget defense spending

Russia’s stagnation from 2013 was made all the worse by the launch of the modernization of the military in 2012. Putin diverted every spare kopek into military spending, and former finance minister Alexei Kudrin got sacked when he objected. It was a seminal moment in Russia’s history where the road forked and Putin chose conflict.

Despite somewhat militarist rhetoric, Russia is actually spending little on defense relative to its Western peers in absolute terms. For the past years the defense spending averaged $50 billion. In his March 2018 address to Federal Assembly, Putin boasted a number of new defense technologies but this appears to contradict the lower-spending trend of recent years.

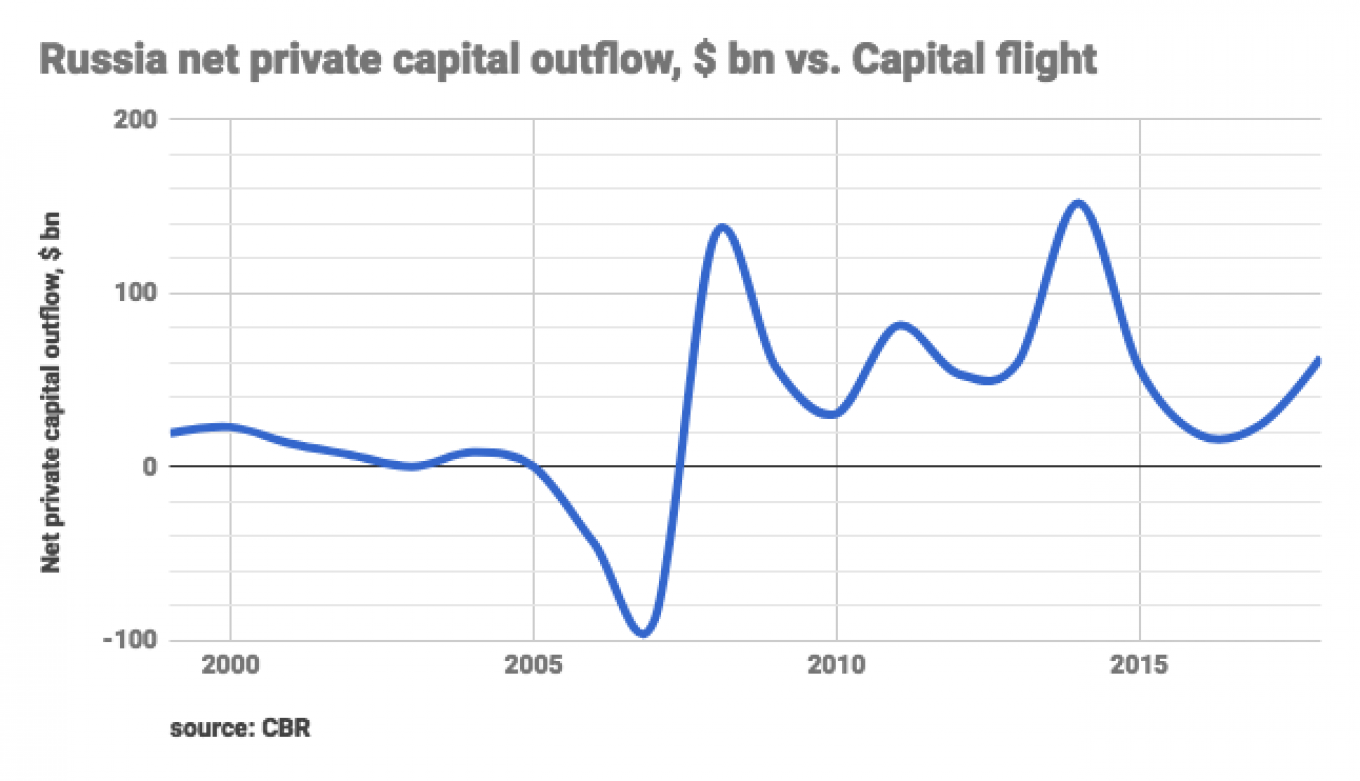

Capital flight

Maybe the most disappointing of all the statistics from the Putin era are those on capital flight. During the 1990s anyone that made any more than they needed sent it abroad. The “transfer pricing” schemes of the leading oil companies where they sold barrels of oil to “independent trading companies” based in Switzerland for $1, which then sold this oil onto the market for $100 have been forgotten today.

One of Putin’s most remarkable achievements was that in 2006 and 2007 he had brought the economy to the point where this capital flight briefly reversed and Russia saw a net inflow of $131 billion as Russian businessmen became optimistic about their own country and started investing. However, as the chart shows the crash of 2008 killed that enthusiasm and the inflow dramatically reversed.

While the outflows in the 90s were about securing personal riches in an offshore haven, the outflows since 2008 have been as much about Russia’s deleveraging as banks and companies pay down the debt they ran up in the boom years.

Financial markets

Another success under Putin has been reform of the financial markets, which have been driven to a large extent by the multiple crises Russia has been through. Again the available data doesn't go back to 2000 but most of the significant changes have been made since 2008.

Banking: During the 1990s and the “wild cat banking” days thousands of small banks were set up that were widely used to hide money from the tax man and whisk cash off shore. The 1998 crisis saw most of the oligarch control banks collapse, which were the keystone in their “financial industrial groups” (FIGs). Banking became a serious business in the boom years, but it wasn't until Elvira Nabiullina took over in 2013 as governor of the Central Bank of Russia (CBR) that a serious clean up of the sector began. Since then she has closed about three banks a week and the number of banks working now has fallen from over 4,500 at its peak to just under 500 today. Nabiullina has introduced a whole raft of other reforms to as the sector becomes easier to regulate.

RTS: The dollar-denominated Russia Trading System (RTS) shows Russia’s rollercoaster ride well. The stock market was established in 1996 before Putin took office and boomed in the noughties with valuations rising by about half every year until the peak of 2,487.92 on May 19, 1998. The index crashed to a mere 38 by October 1999, but had recovered to around 1,500 until the next crisis in 2008 when it crashed again to around 500. In the subsequent years of sanctions and stagnation the index has been range-bound between about 900-1,300. It was only this July after Gazprom announced a surprise large dividend payout that the index broke above 1,400 for the first time in years.

OFZ: Another major financial reform under Putin was the hooking up of Russia’s domestic capital market to the international financial system when it joined the Clearstream and Euroclear payment and settlement systems in 2012. There were foreign investors in Russia’s OFZ before the reform, but only a minority. Money flooded in after the reform until foreign investors owned some $25 billion of the bonds, or 34% of the paper at its peak in April 2018. There was a sanction-induced sell-off last year, but investors have returned in force and currently hold 30% of the outstanding bonds.

'Social'

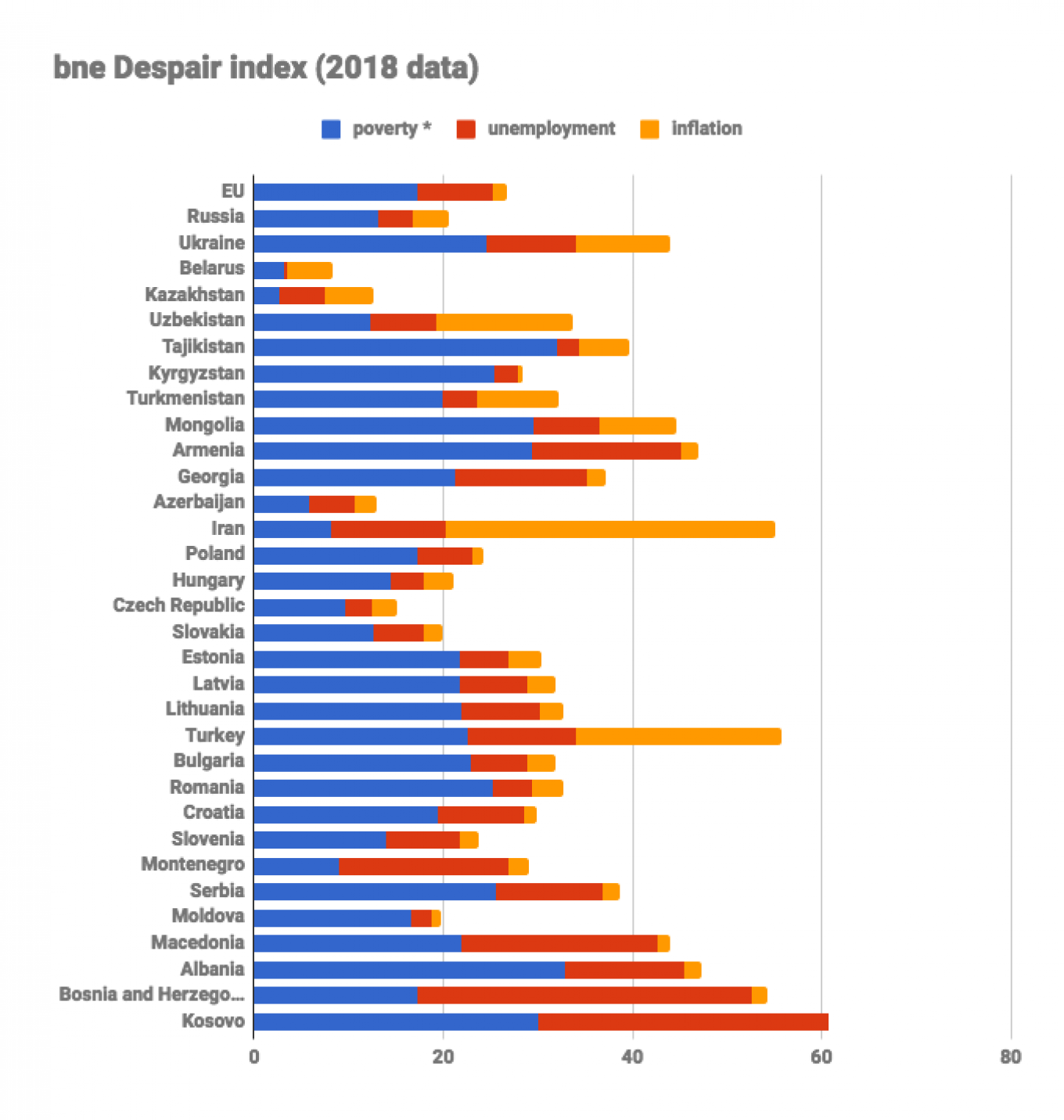

Poverty vs. despair

It is hard to overemphasize the change in the hardships of the 1990s to the relative prosperity of today. However, the rise and fall of poverty during Putin's watch gives some idea. Taking the poverty line as the UN definied $1.90 a day then millions of Russians were in poverty in the 90s. That rapidly fell to nothing in Putin's first two terms of office. If you take the higher Russian official poverty line of 10,753 rubles ($161) then the poverty rate ticked up recently to 14. 3%, but that is on par with most western societies, and even a little less than the bulk of the EU.

We have devised the "Despair Index" which is the sum of the unemployment rate, inflation and the poverty rate, which better captures what life is like in the lower third of society. In the 90s Russia's despair index soared to 2,200, largely thanks to hyperinflation, and was about 10 times higher than any other CEE country. Today Russia's despair index compares favorably with the rest of the developed world.

Russia’s population decline

The chaos of the 90s extracted a terrible price on Russia’s demographics, the effect of which is hitting the working population now. During the boom years the natural population decline was almost halted by Putin’s most successful reforms that were designed to encourage Russians to have more children.

But the bounceback hit peak and the Russian population declined again in 2018 for the first time in a decade as the dent the 90s put the demographic curve hit. But natural population growth has been negative for most of the Putin's time — only net immigration helped Russia to post a total population increase.

Life expectancy

The population may be shrinking but life expectancies have recovered and are now at an all-time high, higher than at any time in the Soviet Union as well.

Life expectancy is rising steadily, explained by lower infant deaths and older people living longer.

Pensioners on the rise

One of the most difficult problems that Putin has to deal with is the aging population. While the “dying Russia” story caught the headlines in previous years it has fallen away as it becomes increasingly clear that all the countries of Europe are facing the same problem. When Putin came to power two workers provided the tax revenues to pay for one pensioner. Today it is closer to one worker paying for one pensioner.

By 2018 the share of people older than working age had risen to 25.4% and was projected to rise to 28.3% by 2028 if the retirement age wasn't raised. Due to the retirement age increase (by five years, to 60 for women and to 65 for men) the share of people older than working age will decline to 22.4% by 2028.

Real disposable income

Putin’s reign can be clearly split into two periods. In the boom years personal wealth soared as real disposable incomes (the spending money left over after paying for food and utilities, adjusted for inflation) rose by 10% or more a year. The 2008 crisis brought the fast growth to an end and after a couple of years of post-shock turbulence the stagnation set in from 2013 onwards and has depressed incomes ever since.

Real disposable incomes have been declining since 2014, and even a shift to new methodology then didn't help to lift reported incomes. However, the picture looks better when you adjust the incomes for purchasing power parity and add in the grey incomes. According to the IMF's estimates for 2018 this means real incomes, including off-the-book payments, are one of the best in the whole of CEE and ahead of several EU countries. These high incomes are the effect of the oil-subsidies that the Kremlin has been pouring into the economy for two decades and the high level of black work and corruption-related income. That extra money puts Russian's income ahead of even Estonia, which has the highest level of income in nominal dollar terms in the region. In practical terms this means that spending money in Russia goes a little bit further than it does in Estonia, but there is a huge difference when Russian's leave the country as Estonia's nominal incomes are close to €2000 a month, whereas Russia's nominal income is a bit less than 800 euros.

'Quality of life'

Murders and suicides

The number of murders and suicides has been falling steadily throughout Putin’s time on the job. Although Putin cannot necessarily take the credit for these trends as they are part of a global trend, it is an indication of general improvement in the mood of society.

Boozing

Russians are famously heavy drinkers and alcohol consumption increased during Putin’s first two terms in office. But the Rosstat figures hide an ongoing switch away from hard spirits like vodka to softer ones like wine and beer, which have become the main tipples in Russia.

The overall level of alcohol consumption has fallen, but the preferred tipple has also changed. Wine overtook vodka as the favorite alcoholic drink in 2017 when a total of 91.9 million deciliters (mndl) of wine were consumed vs 81.1mndl of vodka. If you include sparkling wines in the wine category then wine overtook vodka in 2014. But the significant trend here is the fall in vodka consumption in general. In 2000 Russians consumed a total of 215mndl of vodka — more than two and half times more than they drink today.

Phone ownership

Russians love gadgets and nothing shows the step in the quality of life in Russia better than the rise of mobile phone ownership. The price point of a phone means it is one of the first items the newly comfortable Russian middle class will buy. In 2000 phone ownership soared from 22.3 per thousand people to cover the whole population by 2006 and to reach two phones per person by 2017.

Mortgage loans

Nothing epitomizes the rise of the middle class under Putin like the growth of the mortgage market. Homeownership has been a key policy goal of the Kremlin and Putin has personally actively tried to drive down home loan interest rates. Until recently the state subsides rates over 12% but when they dropped below that level earlier this year the subsidy was dropped. However, in frequent comments to the press Putin called for 10% mortgages, and once that level was passed this year, he is now calling for 8% rates. The first mortgages appeared in around 2003 but only really took off in about 2008. Unfortunately, the CBR date on mortgage lending only goes back to 2006, but for all of Putin’s first term and most of his second the volume of mortgage loans were almost zero.

This article first appeared in bne IntelliNews.

A Message from The Moscow Times:

Dear readers,

We are facing unprecedented challenges. Russia's Prosecutor General's Office has designated The Moscow Times as an "undesirable" organization, criminalizing our work and putting our staff at risk of prosecution. This follows our earlier unjust labeling as a "foreign agent."

These actions are direct attempts to silence independent journalism in Russia. The authorities claim our work "discredits the decisions of the Russian leadership." We see things differently: we strive to provide accurate, unbiased reporting on Russia.

We, the journalists of The Moscow Times, refuse to be silenced. But to continue our work, we need your help.

Your support, no matter how small, makes a world of difference. If you can, please support us monthly starting from just $2. It's quick to set up, and every contribution makes a significant impact.

By supporting The Moscow Times, you're defending open, independent journalism in the face of repression. Thank you for standing with us.

Remind me later.