Since last year’s controlled devaluation, the currency had been surprisingly well behaved. In the last two weeks, however, the markets received a reminder of just how fragile the ruble can be — and how dramatically it is linked to the price of oil.

The wealth of economic news in the last two weeks — both positive and negative — had a hand in keeping the ruble jumping.

There was more good news Wednesday, when the Economic Development Ministry said gross domestic product had shrunk by 10.1 percent in the first half, compared with the 10.2 to 10.4 percent previously forecast by the government, and would end the year at minus 8 to 8.5 percent.

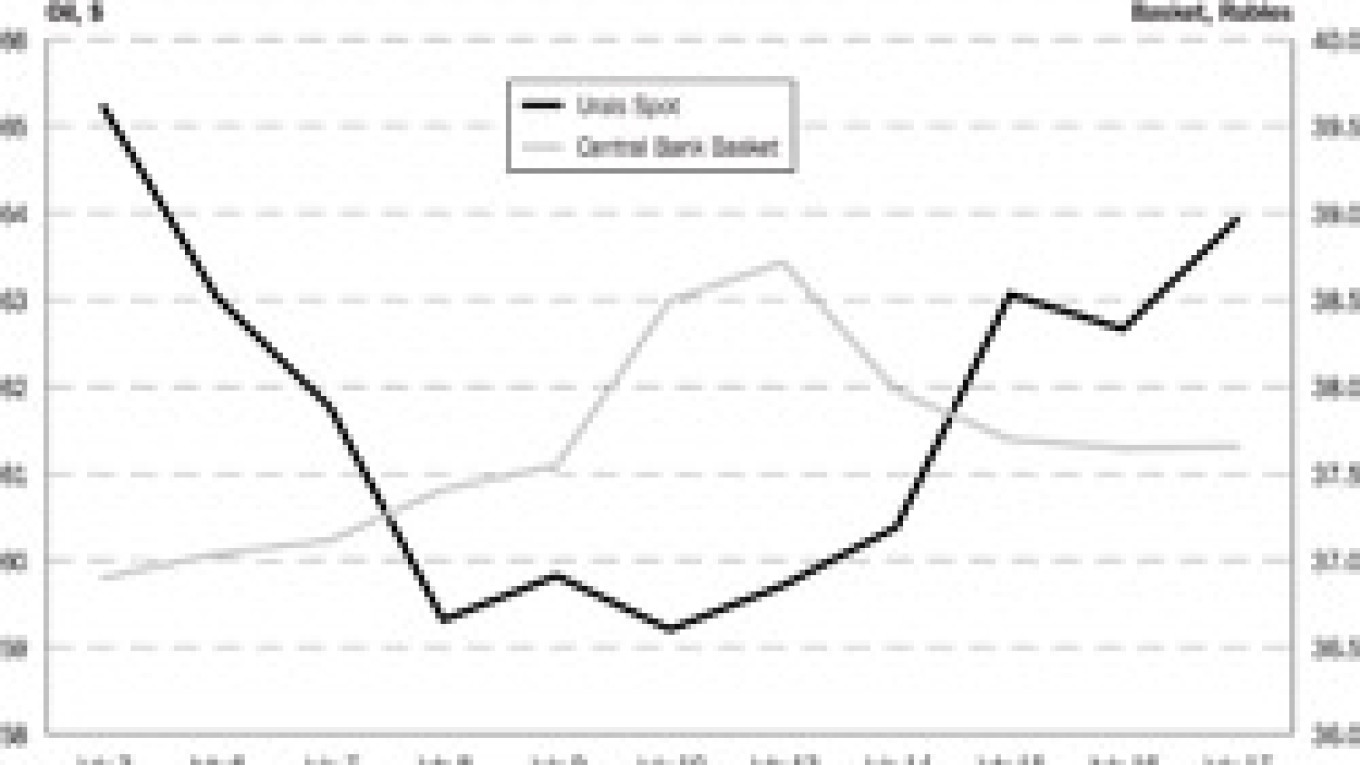

Analysts, however, said oil, which seemed to find ashort-term bottom last week, was what really pulled the ruble back from the edge.

Prices for Urals crude — Russia’s chief export — fell 9.2 percent in the week ending July 10, before gaining back 8 percent in the next five days. The trend was repeated on most global oil markets, with UTI and Brent falling toward $60 but not straying too far past.

But oil was not the only factor responsible for the currency’s volatility.

“As long as there is spare liquidity, the ruble will fluctuate along with oil,” he said.

At $40 per barrel, “the Central Bank would be very near a decision point” on whether to support the ruble, said Citibank chief economist Elina Ribakova.

Alfa Bank said last week that the ruble could fall 16 percent by the end of 2009 to a range of 35 to 38 per dollar if the weaker economy makes it “too expensive and harmful” to support. Such a fall could push the ruble beyond the trading band of 26 to 41 against a basket of dollars and euros set by the Central Bank in January.

This will ultimately put the exchange rate in line with “large swings in fundamentals such as oil prices,” the report said.

“It would be like jumping from one ship to another in the middle of a storm,” said Yevgeny Nadorshin, chief economist at Trust Bank.

A switch away from exchange rate targeting can only come when “derivatives in the local currency market become sophisticated enough to allow participants to adequately hedge their own risk,” rather than having regulators do it for them, Nadorshin said.

A Message from The Moscow Times:

Dear readers,

We are facing unprecedented challenges. Russia's Prosecutor General's Office has designated The Moscow Times as an "undesirable" organization, criminalizing our work and putting our staff at risk of prosecution. This follows our earlier unjust labeling as a "foreign agent."

These actions are direct attempts to silence independent journalism in Russia. The authorities claim our work "discredits the decisions of the Russian leadership." We see things differently: we strive to provide accurate, unbiased reporting on Russia.

We, the journalists of The Moscow Times, refuse to be silenced. But to continue our work, we need your help.

Your support, no matter how small, makes a world of difference. If you can, please support us monthly starting from just $2. It's quick to set up, and every contribution makes a significant impact.

By supporting The Moscow Times, you're defending open, independent journalism in the face of repression. Thank you for standing with us.

Remind me later.